Aclaris Therapeutics ($ACRS)

An intriguing busted biotech situation ($1.15 share price, $81.53m market cap, >$1.5m USD ADTV). Upside estimate of +27-58%, or assuming a six-month resolution, IRR’s of >70%.

The set-up

Aclaris Therapeutics ($ACRS) is a NASDAQ-listed biotech company trading at a ~(54)% discount to it’s last reported net cash value ($2.51 cash per share vs. $1.15 share price), and a (33)% discount to it’s value in our reasonable liquidation scenario.

We believe that following the announcement of a ‘Strategic Review’ on the 16th of January 2024, the company will either be bid on over the next six months, as has occurred in many analogous situations (see $PRDS, $RNEO,$JNCE, $THRX, $RPHM, $RAIN and $KNTE for recent examples), or that the activist shareholders who now hold >20% of the float will catalyze a liquidation (as seen recently with $CYT or $SIOX).

Either scenario materializing would lead to an upside estimate of ~25-50%, or assuming a six-month resolution, IRR’s of >50-100%, with downside capped by the significant existing net cash balance and presence of activist shareholders.

Set-up context

Busted biotech situations can be an extremely fertile place to look for the enterprising value investor. This is primarily due to the ‘air pocket’ that forms following a biotech company announcing a trial failure of one of it’s primary drug candidates. This occurs as the Life Sciences funds that typically dominate the register of such biotech’s rush for the exits, which usually leads to the stock trading at a significant discount to it’s net asset value on the presumption that the existing management team will likely do something reckless with the cash (i.e. M&A) or the company (i.e. reverse M&A) in order to keep their jobs / maintain their commitment to “doing good”.

Since the rapid rise in interest rates, it’s becoming increasingly harder for biotech’s to raise funding as the cost of capital has finally normalized. This has led to >200 US-listed biotech’s trading at a discount to net cash as of 20221. As Jefferies cites, the fact that 25% of the industry is now estimated to trade below cash means that the sector is at levels comparable to the GFC.

When filtering the plethora of busted biotech’s trading below net cash value, it’s important to maintain a strict criteria to avoid what I term the ‘base case’ in these set-ups, which is unfortunately an adverse result for shareholders due to the incentive problems involved (a focus on “science” vs. maximizing shareholder value).

As a generalist who does not have expertise evaluating the technicalities of the science underpinning these companies, we do not award value to any existing IP the company may have, and instead treat this as optionality in the case it is worth something to someone.

The criteria we use to sort through these ideas include:

Liquidity - which affords to opportunity to sell if the facts change

An already announced strategic review

A cash number that is up to date post any restructuring announcement (there is often a lag between the latest financials and a restructuring announcement)

No controlling / blocking shareholder that is motivated by “Science” instead of maximizing shareholder value

The presence of activist or economically-mind shareholders high up on the register whose efforts you can coattail ride upon

A clean balance sheet with easily estimable values for hypothetical liquidation costs (i.e. severance, lease breakage)

Aclaris ticks all of the above.

Set-up context (as mentioned, we are generalists and do not attribute any value to the IP, hence the use of biotech terms below are for purely explanatory purposes)

Aclaris is a clinical-stage biotech company that is / was focused in developing drugs primarily to cure immuno-inflammatory diseases, with it’s primary candidates being: Zunsemetib (ATI-450), ATI-1777, ATI-2138 and the 'Discovery’ platform.

A rough timeline on how we arrived at the situation today is below:

November 13th 2023: Aclaris announced a Phase 2b trial failure of it’s lead drug candidate Zunsemetib (for severe rheumatoid arthritis)2. This led to a >80% collapse of the share price as Aclaris decided to discontinue further development of the program, and cancelled the outstanding trial for the same drug for applications towards psoriatic arthritis.

December 19th 2023: Aclaris progresses another drug trial for ATI-1777 into Phase 2b with a pledge to seek a commercialization partner if the trial is successful (due Jan 2024), and importantly announces a 46% reduction in headcount (from 100 FTE’s) due for completion by June 20243.

January 10th 2024: Shares drop (20)% after the trial for ATI-1777 indicated results that were not statistically superior and in line with existing treatments. Thus, given the competitive market landscape for this drug, this effectively means this drug is in “stand-still” (a further cost reduction for the business)4

January 16th 2024: Strategic review announcement5 where the CEO stepped down, replaced by a co-founder of the business that owns <2% of the shares. I’ve screenshot the most important excerpt below:

January 31st 2024: The Chief Medical Officer is sacked and the remuneration of the Interim CEO is set (which includes full equity award vesting in a Change of Control Scenario)

As market participants have rightly pointed out, the quote in the above strategic review announcement stating “[determining] how to optimally deploy its capital to maximize shareholder return” plus the re-iteration of development plans for it’s remaining R&D pipeline suggests the current management team / BoD are leaning towards M&A with the cash pile or continuing the business as is.

These are no doubt the primary risks for the thesis. But, in our opinion, what underpins our variant perception and where the prospective alpha hopefully derives from, are that these risks should be mitigated by the following...

Enter the activists

Given that ATI-1777 and ATI-2138 are effectively in stand-still as they seek commercialization partners for future FDA trial progression, and that the ‘Discovery’ program has also been practically mothballed, Aclaris is for all purposes a cash-box waiting to be realized.

It may be no surprise then that since almost the entire float has changed hands since the ‘air pocket’ caused by major trial failure in November, several activist-minded shareholders have turned up on this register. This includes renowned broken biotech activists such as Tang Capital (who has recently bid outright on $RNEO, $RAIN, $RPMH, $JNCE, $THRX) and BML, as well as Millenium and Citadel, who own roughly ~6% each. Additionally, Foresite Capital who have recently bid on other broken biotech names such as Theseus ($THRX) and Kinate ($KNTE) own ~6%.

It’s worth noting, however, that Tang and BML Investment Partners acquired their shares at lower levels than the current market price – BML at around $1/share (versus $1.2/share now) and Tang at around $0.6-$0.7/share.

Contingent liability

Before we provide our valuation estimates of each outcome, it is worth noting that another reason that Aclaris may be cuurrently mispriced is due to the existence of a $32.5m contingent consideration liability on the balance sheet as of 09/30/2023. This earn-out was created upon the 2017 acquisition of Confluence (another biotech company), which originally had a book value of $75m6. This earn-out is linked primarily to the trial success of Zunsemenitib and ATI-1777.

Given that the Zunsemenitib trial has now failed, and ATI-1777 is in stand-still, we do not attribute any value to this, and thus do not include it in our valuation estimates.

It is worth nothing that former Confluence equity holders are entitled to consideration from any sale of relevant IP, but given this would be a net positive NPV event, we are treating this as upside optionality.

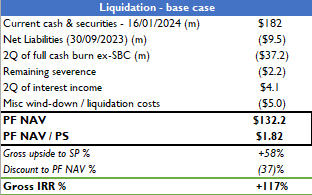

Liquidation scenario (base case)

In the above, we assume a liquidation period of two quarters:

Net liabilities of $9.5m (excluding the contingent consideration liability) adjusted by assets including prepaid expenses and receivables of $20m

Forecasted cash burn $18.5m for the next two quarters (ex-SBC). This is a rough estimate which includes a benefit from the announced 46% reduction in FTE’s and reduced costs from the stalled / failed trials

Severance of $2.2m (in-line with company provided guidance)

$4.1m total in interest income over the next two quarters (roughly 4.5% in line with the past)

Misc wind-down costs of $5m (estimate)

This spits out +58% upside and a very attractive IRR of >100% assuming a 6-month resolution period (IRR’s are still attractive on the basis of >1 year resolution period)

Acquisition target (likeliest scenario)

Estimated $124m of net cash by the end of 1Q24e after deducting estimated cash burn of $18.5m, severance of $2.2m and net liabilities of $9.51m whilst adding back 1Q of interest income on the cash balance at a 4.5% interest rate

Assume Tang (or another party) bids on the company at 85% of PF NAV (Tang’s usual opening bidding price)

This results in attractive upside and IRR’s of >27% and +53% respectively assuming a 6-month resolution period

Liquidation scenario (bear case)

In the above, we assume a liquidation period of four quarters:

Total deduction of all liabilities of $29.5m (excluding the contingent consideration liability) with no offset from the $24m in Other Assets (excluding intangibles)

Cash burn of $20m per quarter for the next four quarters (ex-SBC). This is a rough estimate which includes some benefit for the announced 46% reduction in FTE’s and reduced costs from the stalled / failed trials

Severance of $3m vs. company guidance of $2.2m

$8.2m in interest income over the next four quarters (roughly 4.5% in line with the past)

Misc wind-down costs of $10m (estimate)

This spits out (19)% downside in what I consider the bear case (beyond a totally shambolic announced deal / reverse M&A or the company running the cash balance to zero)

Cash burn testing

The above indicates that assuming $20m of cash burn per quarter, we are looking at 3.7 quarters for the cash balance to fall to the market cap, and two years until cash runs out

Conclusion

I think the risk-reward skew for Aclaris is attractive at these prices. We are seeing both a reduced timeline recently between companies announce strategic reviews and a corporate catalyst occurring. Whilst the share price reactions to a reverse M&A announcement of late have been okayish (see $FIXX, $TALS, $NLTX, $GRPH), I still believe the more likely scenario is ACRS 0.00%↑ being acquired or liquidated over the next twelve months.

Misc

There was 10% short interest reported on Dec 31st 2023. Obviously any news hinting towards a Special Meeting being called by shareholders in aim of a wind-up motion, or a bid on the company would see this covered rapidly.

PWC is the auditor, and the record of both management and the BoD look relatively clean so no there were no “amber flags” raised regarding any fraud risk during DD

Optionality which I haven’t explicitly included in to any calculation of fair value include:

Sale value on the existing IP (not the most remote scenario given on the 5th of December 2023, Sun Pharma just paid $15m to licence IP from Aclaris)

Reverse M&A received well

M&A received well

https://www.bloomberg.com/news/articles/2022-05-04/cancer-drug-developers-trade-below-cash-with-no-respite-in-sight

https://www.sec.gov/Archives/edgar/data/1557746/000155837023018691/acrs-20231113xex99d2.htm

https://investor.aclaristx.com/news-releases/news-release-details/aclaris-therapeutics-provides-corporate-update

https://investor.aclaristx.com/news-releases/news-release-details/aclaris-therapeutics-announces-top-line-results-4-week-phase-2b

https://investor.aclaristx.com/news-releases/news-release-details/aclaris-therapeutics-announces-leadership-changes-and-strategic

https://www.confluencediscovery.com/aclaris-therapeutics-acquires-confluence-life-sciences-inc/

Summary from the 4Q23 10-K (released 27/02/2024):

- Seems okayish - all drugs are on standstill, the contingent liability has unwound, BUT saying "we'll continue the Discovery platform".

- Re-iteration too is that Neal is a "interim CEO" with no timeline on a permanent replacement

- Neal has the option to buy 497k shares at $1.20 - big incentive to get the SP up (also has 142k RSU's). Both vest equally over the N15M with a CoC and BoD award discretionary clause

Foresite has sold it's stake as of 14/02/2024 - not great.